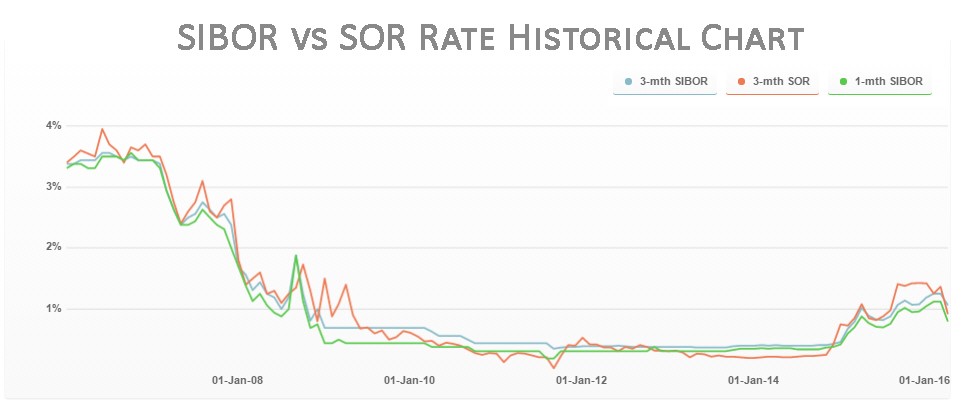

Since the year 2008, homeowners in Singapore have enjoyed relatively low-interest rates.

However, in the year 2015, the interest rates have started to creep upwards. Despite weakening a little from its peak in January 2016, the three-month SIBOR currently stands at 1 percent as of April 2016, more than twice the 0.4 percent level it sat in for the past six years or so.

It is also widely expected that the interest rate will continue its upward movement as the US Federal Reserves has the intention of raising the US interest rates by the end of this year or early 2017.

Hence, it is timely for homeowners who are still servicing housing loan(s) to relook into refinancing. In this article, we have listed 5 tips for refinancing your housing loan.

5 Tips for Refinancing

- Track your loan’s lock-in period and prepare for the switch

- Repricing instead of Refinancing

- Refinance before 30 June 2017 (for investment property loans)

- Watch out for LTV limits

- Stress Test to Decide Fixed or Floating Loan Package

1

No.1: Track your loan’s lock-in period and prepare for the switch

Be it fixed or floating rates, in most loan packages if not all, after the initial lock-in period of low rates, the interest rates will go higher. Below are examples of loan packages that shown a significant increase in interest rate after you complete your 3rd year (which is commonly aligned with the lock-in period):

For fixed rates, after the lock-in period, the rates might become floating and definitely higher rates.

Year 1:

1.99% p.a. Fixed

Year 2:

1.99% p.a Fixed

Year 3:

1.99% p.a Fixed

Thereafter:

FHR18 + 1.80% p.a

*Fixed Deposit Home Rate (FHR18) refers to the prevailing 18 months Singapore dollar fixed deposit interest rate of DBS Bank for amounts within $1,000 to $9,999 or such other sum as we may specify. The FHR18 is transparent and less volatile compared to a market benchmark rate such as the SIBOR. The current FHR18 (as of 2 May 2016) is 0.60% p.a.

For floating rates, after the lock-in period, like fixed-rate packages, the interest rates will spike.

Year 1:

3-month SIBOR + 0.80% p.a.

Year 2:

3-month SIBOR + 0.80% p.a

Year 3:

>3-month SIBOR + 0.80% p.a.

Year 4:

3-month SIBOR + 1.25% p.a.

*SIBOR stands for Singapore Inter-bank Offered Rate. It is the average rate derived from the lending and borrowing rates between financial institutions and announced by The Association of Banks in Singapore on a daily basis. It is mainly affected by two factors, namely the US Fed interest rates and liquidity in Singapore banking sector.

Tip by Realila

We would advise homeowners who are still servicing their loan to set a reminder 6 months prior to the expiration of their lock-in period. In this 6 months, you can do research on the various loan packages that are available in the market. So, when the time has come that your lock-in period has expired, you can make a well-informed decision to stay onto your existing loan package or switch to a better loan package.

2

No. 2: Repricing instead of Refinancing

Consider repricing instead of just refinancing. In practice, when you took up a new loan package with your existing mortgage bank, you are doing a repricing. In other words, refinancing with your existing bank.

Tip by Realila

As mentioned in the 1st point, you should start your research for available loan packages from other banks before you reach your lock-in period. Once you have found an attractive loan package from another bank, you may then negotiate with your current bank for a better deal. This will save you from incurring additional processing and legal fees. If the loan package is so attractive that your current bank cannot match or compete, you may then consider jumping ship after weighing in the additional processing and legal fees.

3

No. 3: Refinance before 30 June 2017 (for investment property loans)

Since the introduction of Total Debt Servicing Ratio (TDSR) on 29 June 2013, it has made refinancing harder for some. In short, TDSR limits a borrower’s mortgage repayment plus their other monthly debts obligations (like a car loan instalments, credit bills, personal loan etc.) to a cap of 60% of their monthly income. There are some exemptions for homeowners who was granted OTP before 29 Jun 2013 and he/she is occupying the property that he is refinancing. The details of exemptions can be found in this link: http://www.mas.gov.sg/news-and-publications/media-releases/2014/mas-broadens-exemption-from-tsdr-threshold.aspx.

Tip by Realila

If you are refinancing an owner-occupied property which was granted OTP before 29 June 2013, you are more or less spared from the brunt of TDSR. However, we still encourage you to practice financial prudence so you would not stress over unnecessary debt obligations.

For refinancing of investment property loans, you are given a transition period until 30 June 2017 to manage your debt obligation. Before 30 June 2017, you can still refinance your investment property loans above the 60 percent threshold capped by TDSR. However, you must fulfill the set of criteria set by MAS. In the event that you have over-leverage, we would recommend you to take this transition period to reassess and adjust your property portfolio. You should be aware that the low-interest rate the market is enjoying now will not last forever. When the interest rates rise, you may face higher mortgage repayment. At that point of time, after the transition period, you may have great difficulties refinancing and cash flow may become an issue.

4

No. 4: Watch out for LTV limits

In January 2013, MAS lowered the Loan-to-Value (LTV) limits for housing loans to individuals with one outstanding housing loan from 60% to 50%, and to individuals with two or more outstanding housing loans from 60% to 40%. Loans with longer tenure faced even tighter LTV limits. Lower LTV limits also apply to a loan granted for the purchase of a residential property where the loan period extends beyond the retirement age of 65 years or the loan tenure is more than 30 years.

Tip by Realila

For homeowners who are servicing 2 or more housing loans, it is wise to quickly pay up at least 1 housing loan. Else, you may not be able to refinance due to the lower LTV limit. For those couples who are financial-strong, you may “de-couple” to “raise” the LTV limit for the 2nd loan.

5

No. 5: Stress Test to Decide Fixed or Floating Loan Package

This is a very common question asked by homeowners when deciding the loan package to sign up.

In general, homeowners who are risk-averse and want a fixed monthly repayment, fixed rates will be the best option, but the rates might not be the lowest.

For homeowners who are less risk-averse, you can consider floating rates where onset or in today’s market condition (as of 2 May 2016), the interest rates are lower. However, the flipside is that floating rates are more volatile, meaning the monthly repayment fluctuates and not suitable for those who are faint-hearted.

Tip by Realila

To decide which package is suitable for you, we recommend that you do a stress test to determine how much you can afford if floating rate increases to a certain level. If you are able to accept a floating rate at a high level (or what we commonly called worst-case scenario, typically 3.5% – 4.5%), you may then consider a floating rate package to enjoy the current low-interest rate.

Above are the 5 great tips we have for refinancing your housing loan. If you have other good tips to share with our readers, do write to us at hello@realila.sg or Whatsapp us at +65 81513343.