Suitable reading for property buyers looking to use a housing loan to buy a property.

Last week, we received feedback from our user Mr. Zhao. He mentioned that his banker told him that he would be able to borrow up to S$4,000,000 to purchase his next property. However, when he used Realila Property Budget Calculator, he found out that he could only purchase a property not exceeding S$900,000 in value.

Alarmed by the huge discrepancies, we probed deeper and realized that the assessment done by the banker took only into account his income. In contrast, Realila Property Budget Calculator takes into account all information on his financial profile. This includes factors such as the funds he intended to use for his next purchase, his outstanding monthly loan obligations, his current property portfolio etc, so as to generate a complete assessment of his budget.

Although TDSR and tightening of Loan-to-Value (LTV) has been introduced years back and was written by many industry bloggers, Mr. Zhao’s feedback prompted us to share (recap) with you, our readers, how Total Debt Servicing Ratio (TDSR) & Loan-to-Value (LTV) can affect your budget for your property purchase.

TOTAL DEBT SERVICING RATIO (TDSR)

Total Debt Servicing Ratio (TDSR) is a framework introduced on 28 June 2013 to “strengthen credit underwriting practices by financial institutions” and “encourage financial prudence among borrowers”. It is the percentage of your income that can go toward servicing your home loan, after taking into account your other debts like credit card debt, car loan, personal loan etc. It is a permanent structural reform that all banks and financial institutes must follow when assessing and approving housing loan applications. Here’re the key points of TDSR:

- Total Debt Servicing Ratio Capped at 60%

- All Variable & Rental Income are subjected to 30% Haircut

- Value of Eligible Financial Asset is subjected to 30 to 70% Haircut

- Introduction of Income-Weighted Average Age

- Stress test at 3.5% or 4.5% interest rate

- All Owners to be Borrowers / Guarantors to be Joint-Borrowers

- Greater Stringency in the Application Process

Separately, we will have a summary on the current (as of 26 March 2016) the Loan-to-Value Limits.

60%

Total Debt Servicing Ratio Capped at 60%

In the past, Debt Servicing Ratio is used by banks and financial institutions to assess how much of your income can be used for servicing your debts, and the percentage guide used is 50% of your income. For a moment, we may cheer at the increase of capped from 50% to 60%. However, TDSR (unlike DSR) requires that your monthly mortgage repayment together your other monthly debts obligations like car loan, personal loan etc. cannot exceed more than 60% of your monthly income.

How does this affect you?

If you are totally debt free, this is a piece of good news to you. Your monthly mortgage repayment against your income is now officially increased to 60% of your monthly income. However, if you have been splurging using your credit card, financing your car and/or have taken some personal loan, your monthly mortgage repayment allowed to finance your property will be affected. In other words, the amount of housing loan you can get from the banks or financial institutions will be reduced.

For example, if you are earning a good income of S$10,000 per month and are debt-free, you could secure a housing loan where your monthly mortgage repayment is not more than S$6,000 (60% of S$10,000). However, if you have other financial obligations (credit loan, car loans etc.) which, perhaps, make up to S$2,000 per month, the monthly mortgage repayment allow will be S$4,000 (S$6000 – S$2,000). Given you can only secure a housing loan that caused S$4,000 monthly repayment, the quantum loan you can be secured is in turn reduced.

With the new TDSR ruling, some people try to maximize their TDSR ratio by delaying their purchase of big ticket items like car, appliances etc. before purchasing their property. However, it is recommended that you exercise prudence in your financial obligations and live a lifestyle within your means =)30percent

All Variable & Rental Income are subjected to 30% Haircut

In the TDSR framework, variable incomes of below nature will be subjected to 30% haircut, i.e. it will be treated at 30% less than it actually is. These include:

- Commissions from sales

- Rental income from your properties (stamped tenancy agreement with remaining rental period of least 6 months)

- Monthly bonus

- Income from side-projects or freelance work

How does this affect you?

Ouch! If your total income is made up of substantial amounts of variable income like bonuses or rental income or you are paid in commission, the amount of housing loan you can get from the bank will be greatly reduced. This is because only a maximum of 70% of your average monthly variable income in the past 12 months will be taken into consideration. It’s the same for rental income – it will suffer a 30% haircut when taken for loan assessment.

asset

Value of Eligible Financial Asset is subjected to 30 to 70% Haircut

If you are depending on your existing financial assets like fully paid properties, equities, and other assets which used to be considered for Asset-based lending (ABL), these assets are now subjected to a haircut of 0% – 70% depending on asset type and pledged status. Then, the discounted value of the assets will be amortized over 4 years as income streams for computation.

How does this affect you?

This usually affects individuals who are unemployed (or typically, retirees) and High Net Worth Individuals (HNWIs), as they usually have accumulated a good amount of financial assets. But these assets can now only be converted to much smaller “income streams”.

Anchor Text for IWAA

Income-Weighted Average Age

Gone are the days where the younger or average age of all borrowers are used to calculate the loan tenure. Income-weighted average age will now be used for the joint borrower. Below example shows how this “income-weighted average age (IWAA) for joint borrower” comes into play:

Computation of IWAA

Borrower A, age 30 earns S$ 3,000 per month

Borrower B, age 40 earns S$ 5,000 per month

Computation of Tenor

![]()

So to achieve max Loan-to-Value (LTV), the loan tenure is capped at 28 years (i.e. 65 years – 37 years)

So how does it affect you?

In the past, there are scenarios where older applicants (e.g. 55 years old) earning a significantly more (e.g. S$15,000 per month) are able to obtain a higher loan tenure by roping in their younger children (e.g. 25 years old) earning around S$ 2,000 per month to lower their loan age to 40 years old (average of 55 & 25). However, this is no longer possible with the implementation of the TDSR framework.

stresstest

Stress test at 3.5% or 4.5% interest rate

In the past, banks calculated one’s DSR based on assumed percentage of around 2.5% to 3%, slightly higher than the current interest rate. However, with TDSR, the assessment/stress test has been standardized across the board by MAS and bank has to assess based on a higher interested rate of 3.5% for residential property & 4.5% for non-residential property.

How does it affect you?

Despite a low-interest rate environment today (23 March 2016), the loan that can be extended to you is calculated at 3.5% for residential property & 4.5% for non-residential property. This “stress test” protects you from the potential increases in interest rates. Henceforth, you can worry less that you will be badly affected by rising interest rate in the future as the bank has extended the loan to you based on higher interest rate of 3.5% or 4.5%.

Anchor Text for Borrower

All Owners to be Borrowers / Guarantors to be Joint-Borrowers

Every borrower must be a mortgagor, and a guarantor must also be a borrower. And borrowers will be subject to the loan-to-value regulations.

How does it affect you?

These effectively clip the wings of borrowers and guarantors as they will have a property and loan with their name in it respectively. This prevents individual from acting as guarantor simply to help a borrower increase his loan amount – this helpful individual will now have a property and/or loan in their name, affecting their future property purchase as they will be subjected to ABSD and will have lower borrowing LTV.

Application

Greater Stringency in the Application Process

Before this framework was implemented, one could get away by claiming lower debt obligations. Now, the banks are required to run stringent checks during the application process and documentation is now demanded as proof and also for wider categories of issues.

How does it affect you?

You are now required to provide banks with your documents (past credit card statement, car loans statement etc.) to validate your financial status. This would make the application process more tedious than before.

Anchor Text for LTV

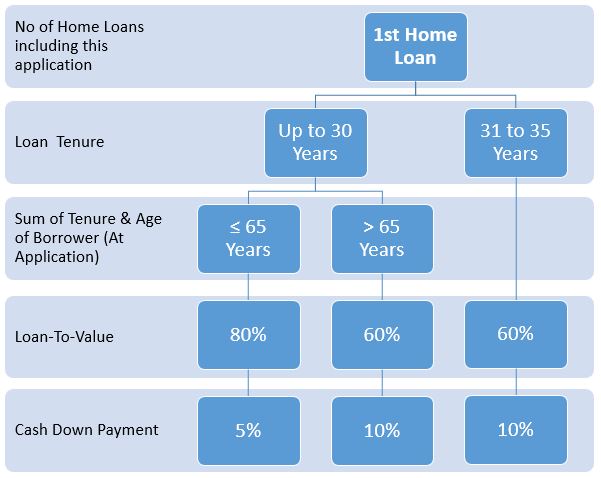

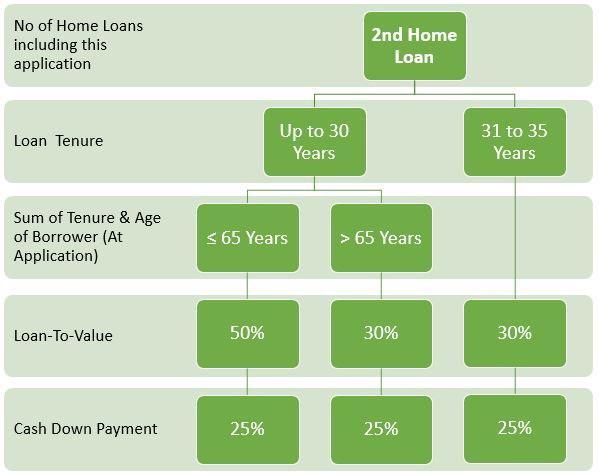

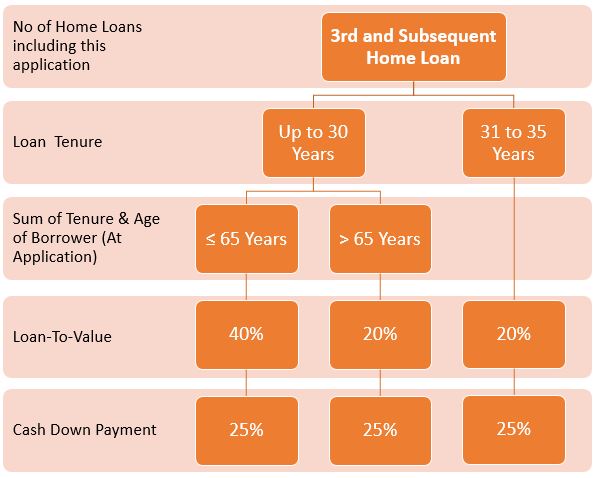

TIGHTER LOAN-TO-VALUE RATIO (LTV)

Having noticed a trend towards larger loans being issued by banks and financial institutions, the government has also introduced and tightened the loan-to-value ratio. The table below shows the latest LTV limits for:

- 1st Home Loan

- 2nd Home Loan

- 3rd and Subsequent Home Loan

Anchor Text for 1st Loan

Anchor Text for 2nd Loan

Anchor Text for 3rd Loan

Anchor Text for Case Study

Case Study

Let’s go back to Mr Zhao’s scenario. So let’s start by assuming Mr.Zhao’s total income is $35,000. Based on his income (no loan etc.) only, he will be able to secure a housing loan of up to around S$4,000,000.

However, as he is currently financing a mortgage loan, his LTV is dropped to 50% (his total loan tenure will not extend beyond 65 years old). With Cash/CPF of S$550,000 to purchase his next property, and LTV ratio of 0.5, he would only be able to purchase a property up to S$1,100,000.

Furthermore, as this is his 2nd property, he will have to pay ABSD of 7% on the purchase price and, after factoring other costs involved in buying his 2nd property, the maximum buyable property value is now S$900,000. You may ask what about his TDSR. For his case, his TDSR ratio was around 26%, but due to a much tighter LTV, the TDSR did not affect his budget for his property purchase.

With the introduction of TDSR, ABSD & LTV, it may take up a considerable amount of your time to work out your budget for your property purchase. Thankfully, you can now work out your property budget in minutes with Realila Property Budget Calculator. The calculator is free to use and it takes away all of the guesswork to find out your purchase power. If you are looking to work out your TDSR or ABSD, you may try out these calculators too: TDSR calculator & ABSD Calculator.

Do hope the above articles help you to better understand the TDSR framework & Tightened LTV. If you have any questions or feedback, do feel free to write to us at hello@realila.sg. Or, simply share your thoughts regarding TDSR be leaving us your comments below.

P.S: We would like to thank Mr. Zhao for his feedback and compliments once again.

*Note: For Mr. Zhao’s case, we are assuming his income and available CASH/CPF. We are unable to access the exact information he has input into our system as all information input into our system is encrypted. During our conversation, he has informed us that his housing loan can go up to S$4,000,000 and question why Realila’s Property Budget shows that he can only afford property of S$900,000. With that piece of information, we have worked backwards to get the numbers to present the case study to him and to you. Permission has been given from Mr. Zhao to published his case study for your reference.

Buying a Property?

Work out your budget with Realila Property Budget Calculator today.

Takes into consideration your income, loans, property portfolio, ABSD payable, Loan-to-Value, TDSR etc.

It’s FREE, RELIABLE & SECURE.